How I Cut Costs When Illness Hit Hard — A Real Talk on Financial Survival

One minute I was fine, the next I was on medical leave with bills piling up. A sudden illness doesn’t just hurt your body—it hits your wallet too. I learned this the hard way. What started as a routine check-up turned into unexpected costs and financial stress. But through trial, error, and some smart moves, I found ways to reduce expenses without sacrificing care. This is how I protected my finances when life threw a curveball. It wasn’t about cutting corners or skipping treatments—it was about making informed choices, using resources wisely, and staying calm under pressure. Many women in their 30s to 50s face similar challenges, often managing family needs while dealing with their own health setbacks. This story is for anyone who has ever worried about how to pay the next bill while focusing on getting better.

The Shock of Sudden Illness: When Health Meets Financial Crisis

Imagine waking up one morning feeling off—just a little fatigue, maybe some lingering discomfort. You brush it off at first, thinking it’s stress or a minor bug. But within weeks, doctor visits pile up, tests are ordered, and suddenly you’re handed a diagnosis that changes everything. That was my reality. What began as vague symptoms led to a chronic condition requiring ongoing treatment and months of recovery. The physical toll was difficult, but the financial strain nearly broke me. I had savings, yes—but not enough to cover months without income and rising medical costs. In just three months, my emergency fund was drained. Lost wages, high-deductible insurance, and surprise charges added up faster than I could track them. The emotional weight of this double burden—health and money—was overwhelming. Studies show that financial stress can worsen health outcomes, slowing recovery and increasing anxiety. I felt trapped: every medical decision came with a dollar sign attached. And I wasn’t alone. Millions of working adults, especially women managing households, face this same crisis each year. The truth is, most people are one serious illness away from financial instability. Emergency funds often fall short because they’re built for car repairs or job loss, not long-term medical leave. Without a plan, even a treatable condition can spiral into a financial disaster. This experience taught me that financial resilience isn’t just about saving—it’s about preparing for the unexpected with clear strategies and emotional strength.

Rethinking Medical Costs: Smart Choices Without Sacrificing Care

When illness strikes, every medical decision carries financial weight. The instinct is to accept whatever treatment is recommended, fearing that questioning costs might mean compromising care. But I learned that being informed doesn’t mean being reckless—it means being responsible. One of the first steps I took was to request itemized bills from every provider. What I found was surprising: duplicate charges, unexplained fees, and services I never received. By disputing these errors, I reduced my out-of-pocket costs by nearly 15%. I also discovered the power of in-network providers. Switching to doctors and labs covered under my insurance plan cut my lab fees in half. It wasn’t about choosing cheaper care—it was about choosing smarter care. Another key move was seeking second opinions, not just for diagnosis but for cost. One specialist recommended an expensive imaging test, but a second doctor suggested a less costly alternative with the same diagnostic value. That single change saved me over $800. I also learned to ask questions: Is this test absolutely necessary? Are there generic medications available? Can I do this outpatient instead of inpatient? These conversations weren’t confrontational—they were collaborative. Doctors respected my engagement, and many offered lower-cost options I hadn’t considered. Negotiating bills directly with hospitals also made a difference. Many institutions offer payment plans or financial assistance programs, but you have to ask. I set up a no-interest payment plan that allowed me to spread costs over ten months without penalties. The lesson? Reducing medical expenses isn’t about avoiding care—it’s about advocating for yourself, understanding your options, and using available tools to protect your finances while staying healthy.

Income Protection: Bridging the Gap During Recovery

Losing income during illness is one of the most stressful aspects of a health crisis. For many women, especially those in caregiving roles, the idea of stopping work—even temporarily—feels impossible. I was no different. My job provided stability, health benefits, and a sense of purpose. When I had to go on medical leave, the loss of income created immediate pressure. But I quickly realized that waiting for savings to run out wasn’t the only option. I explored short-term disability benefits through my employer and found I qualified for 60% of my salary for up to six months. It wasn’t full pay, but it covered essentials like rent, utilities, and groceries. The key was acting fast—applications can take weeks to process, and delays mean lost payments. I also reviewed my company’s sick leave policy and combined it with vacation days to extend paid time off. This bridge helped me avoid dipping into retirement savings. For those who can manage light work, freelance or remote opportunities can provide extra income without physical strain. I started doing light administrative work a few hours a week when I felt up to it. It wasn’t much, but it helped cover prescription costs and kept me mentally engaged. Some women I’ve spoken with have turned to online tutoring, virtual assistant work, or selling handmade goods during recovery. The goal isn’t to overwork—it’s to create small, sustainable income streams that reduce financial pressure. Government programs like Social Security Disability Insurance (SSDI) are also options for long-term conditions, though approval can take months. The takeaway? Income protection isn’t passive—it requires knowledge, planning, and action. By understanding available benefits and exploring flexible work options, you can maintain some financial flow even when your body needs rest.

Budget Overhaul: Trimming the Fat Without Losing Stability

When income drops and expenses rise, rethinking your budget isn’t optional—it’s essential. I sat down with my monthly spending and categorized everything: needs, wants, and obligations. The goal wasn’t to live in deprivation but to redirect funds where they mattered most. First, I paused non-essential subscriptions—streaming services, gym memberships, and magazine renewals. That saved nearly $120 a month. I also called my internet and phone providers to negotiate lower rates, explaining my situation. Both companies offered temporary discounts, reducing my bill by 30%. Housing costs were the biggest challenge. I talked to my landlord about a short-term rent reduction, framing it as a temporary request due to medical leave. To my surprise, he agreed to a two-month deferral, which gave me breathing room. For those with mortgages, loan forbearance programs may be available through lenders. Utilities were another area for savings. I switched to energy-efficient lighting, reduced heating and cooling usage, and qualified for a low-income assistance program that lowered my electric bill. Groceries required careful planning. I switched to store brands, bought in bulk when possible, and used digital coupons. Meal prepping helped avoid costly takeout during low-energy days. I also postponed big purchases—no new furniture, electronics, or vacations. These weren’t permanent cuts but strategic pauses. The key was flexibility: I reviewed my budget every two weeks and adjusted as my health and income changed. This approach kept me from feeling trapped. Instead of panic, I felt control. Over six months, these changes saved me over $3,000—money that went toward medical co-pays and essential living costs. A budget overhaul during illness isn’t about sacrifice—it’s about smart reallocation, temporary adjustments, and protecting your financial foundation when you need it most.

Navigating Insurance: Making It Work for You, Not Against You

Insurance is supposed to protect you, but during a health crisis, it can feel like another obstacle. Claims get denied, coverage limits kick in, and paperwork piles up. I quickly learned that understanding my policy wasn’t optional—it was survival. I started by reading my insurance documents thoroughly, focusing on deductibles, co-pays, out-of-pocket maximums, and pre-authorization requirements. Knowing these details helped me anticipate costs and avoid surprises. When a claim was denied for a specialist visit, I didn’t accept it. I filed an appeal with supporting medical records and a letter from my doctor explaining the necessity of care. After three weeks, the decision was reversed, and I was reimbursed. Persistence paid off. I also discovered that many hospitals offer financial counselors—trained professionals who help patients understand billing, insurance, and assistance programs. Meeting with one saved me hours of confusion and uncovered a charity care program I qualified for. Another critical step was ensuring all providers billed my insurance correctly. I confirmed my coverage status before every appointment and followed up to make sure claims were submitted on time. Delays often led to denied claims, so staying on top of this was crucial. I also learned about Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs), which allow pre-tax dollars to be used for medical expenses. If you have access to these, they’re powerful tools for reducing out-of-pocket costs. For those without employer-sponsored plans, marketplace insurance plans vary widely in coverage—comparing them carefully during open enrollment can prevent gaps in protection. The bottom line? Insurance only works if you actively manage it. Being informed, asking questions, and advocating for coverage turns a confusing system into a valuable resource. It’s not about fighting the system—it’s about using it to your advantage.

Preventive Planning: Building a Financial Safety Net Before Crisis Strikes

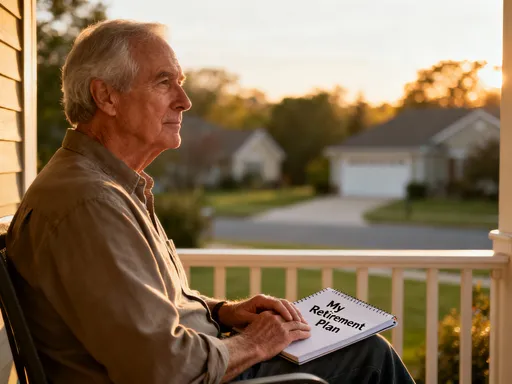

The best time to prepare for a financial crisis is before it happens. That’s a lesson I wish I’d learned earlier. Once I recovered, I committed to building a stronger financial safety net. The first step was rebuilding my emergency fund—not just for job loss, but specifically for medical emergencies. Financial experts often recommend three to six months of living expenses, but for health-related risks, I now aim for eight to twelve months. This buffer covers not only daily costs but potential medical bills and lost income. I automated monthly transfers to a high-yield savings account, treating it like a non-negotiable bill. Next, I reviewed my insurance coverage. I upgraded to a plan with a lower deductible and better specialist access, even if the premium was slightly higher. I also secured short-term and long-term disability insurance through my employer—a step many overlook until it’s too late. Disability insurance replaced a portion of my income when I couldn’t work, and having it in place would have reduced my stress significantly. I also created a personal financial checklist: updated beneficiaries, organized medical and insurance documents, and identified potential income sources in case of illness. For homeowners, umbrella insurance adds extra protection. For parents, life insurance ensures family stability. These aren’t morbid thoughts—they’re practical safeguards. I also started tracking my health and medical history in one digital file, making it easier to share with providers and insurers when needed. Preventive planning isn’t about fear—it’s about empowerment. By taking small, consistent steps now, you build resilience that protects your family, your health, and your peace of mind. The goal isn’t perfection—it’s progress. Every dollar saved, every policy reviewed, every document organized is a step toward greater security.

Mindset and Money: Staying Calm to Make Clear Financial Decisions

During my illness, I realized that financial survival isn’t just about numbers—it’s about mindset. Stress clouds judgment. When I was overwhelmed, I made impulsive decisions: skipping a doctor visit to save money, then needing more expensive care later. Anxiety led me to avoid opening bills, which only worsened the problem. I learned that protecting my mental health was just as important as managing my budget. One of the most helpful tools was pausing before making financial decisions. Instead of reacting immediately, I gave myself 24 to 48 hours to reflect, gather information, and consult a trusted friend or advisor. This simple habit prevented costly mistakes. I also sought emotional support. Talking to a counselor helped me process fear and guilt about money. Joining a support group connected me with others who understood the dual burden of health and finance. We shared tips, resources, and encouragement. Knowing I wasn’t alone made a difference. I also practiced daily grounding techniques—deep breathing, journaling, short walks when possible. These small acts restored a sense of control. I stopped seeing myself as a victim of circumstance and started seeing myself as a problem-solver. This shift in mindset changed everything. I became more proactive, more organized, and more confident in my choices. I stopped hiding from bills and started managing them. I stopped feeling shame about needing help and started asking for it. Financial decisions became less emotional and more strategic. The lesson? Mental resilience fuels financial resilience. When you’re calm, you think clearly. When you think clearly, you act wisely. And when you act wisely, you protect not just your wallet, but your well-being.

Recovering from a sudden illness isn’t just about healing the body—it’s about stabilizing your entire life. By taking control of costs, leveraging available resources, and planning ahead, you can survive the financial shock and emerge stronger. This experience taught me that resilience isn’t just physical; it’s financial, emotional, and deeply personal. And with the right moves, you can protect what matters most—your well-being and your peace of mind. For women managing families, careers, and health, the stakes are high. But so is the power to act. You don’t need a perfect plan—just a few smart steps. Start today: review your insurance, build your emergency fund, and know your rights. The goal isn’t to avoid illness—it’s to face it with strength, clarity, and confidence. Because when life throws a curveball, your preparation can make all the difference.